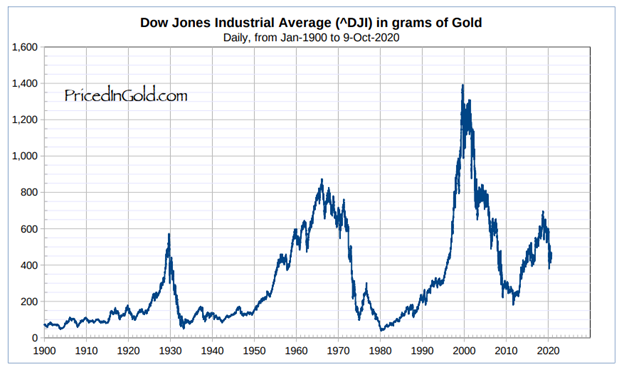

Now for more news, your stock market investments may be worth under one-third of their value in 2000. Gasp. Yes, the gain of the last 20 years has been illusory. For sure, some countries and some market sectors have done better than others, but for the USA main index, this is exactly what has happened.

(Chart: DJIA priced in ounces of gold)

Even if large corporations prosper, the US DJIA stock index and gold have a history of a near meeting when a financial crisis bottoms out. Currently, the DJIA is worth around 14 times the price of an ounce of gold. In 1932 and 1980, just over one ounce of gold bought the DJIA. Whether a large stock market crash achieves that, as was the case in 1932, or inflation pushing up the gold price, as was the case in 1980, it may be destined to happen again.

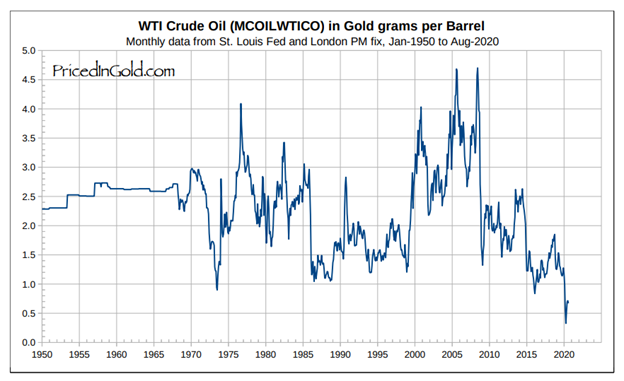

Oil is still one of the biggest building blocks of life. Regardless of whether you now work from home instead of driving to work every day in the gas-guzzler or not. It’s used in everything – fuels, plastics and pharmaceuticals, to name a few. In fact, if you now work from home, chances are you’re turning up the winter thermostats a bit more often than you would at work. You’re probably also buying a lot more food from the supermarket, most of it encased in plastic packaging. Even if your heating system is not oil-based, oil remains one of the main fuels available for generation of electricity, and could well do so for many, many years, regardless of how many windmills they build.

So, the good news. You’ll be pleased to hear is that oil is at an all-time low, when measured against gold. Luckily enough, since with your earnings being one-sixth of the 1970 value, you may not be able to afford to keep the house warm or drive a car otherwise. Any apparent price rises you see at the pumps are merely an inflation of your fiat currency.

Now for the bad news, can it continue?

Maybe not. For many years, gold and Oil actually maintained a near 10:1 ratio relationship.

(Chart: Gold/Oil ratio 2010 to 2020)

As the chart shows, this relationship has become distended as a result of the Corona crisis. There’s now a near 50:1 relationship as of August 2020. This may imply oil is actually quite cheap, gold is expensive, or that the ratio no longer holds. There has been a multitude of media articles heralding the death of oil. However, it seems to have missed the attention of many that all of this data – everyone’s Facebook posts, Instagram images, or cloud software solution is stored on a server somewhere that requires electrical power to run. For sure, in the case of one Instagram post, that electrical consumption is miniscule, but multiply it across a world of 7 billion people, and you get an idea now of the immense electrical power required. Oil, natural gas, and coal are still heavily used in electrical power generation across the globe.

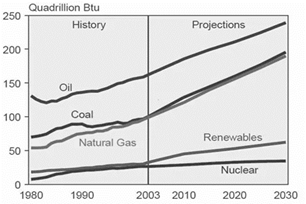

(Chart: Actual and predicted power sources to 2030)

The eagle-eyed among you may have spotted the chart dates from 2003. This was deliberate since more recent data shows it to be correct. If so, the future trend for oil consumption is still upward.

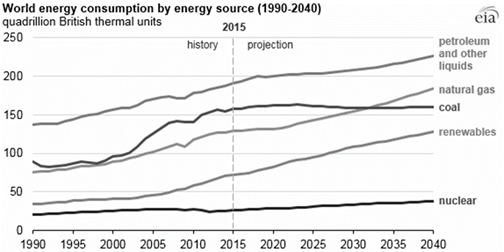

(Chart: Energy consumption to 2040)

So, and this is only a question, not investment advice, maybe oil itself is not finished yet as an investment. If not, could it revert back to the 10:1 ratio with gold and if so, at what price for both?

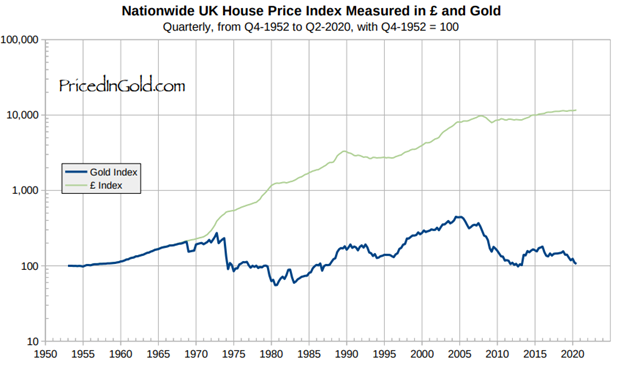

Now for some big news. If you live in the UK, your house topped in value in 2005 and has been falling ever since. In fact, it’s now about one-quarter of what it was worth then. What? I hear you say. Okay, yes, in fiat currency units it has gone up, but measured in gold, it has fallen dramatically.

Measured this way, house prices are very close to the 1950 mean. However, with the Corona crisis still in full swing, employment uncertainty for many and wages still at one-sixth of their 1970 value, it’s entirely possible the market could still have a lot further to fall. Conversely, if something happens to get wages closer to the mean or inflation rises, well, they could easily move upwards in fiat currency terms especially.

In this case, the housing market is hard to exit, unless you prefer the uncertainty of renting. Everyone needs to live somewhere.

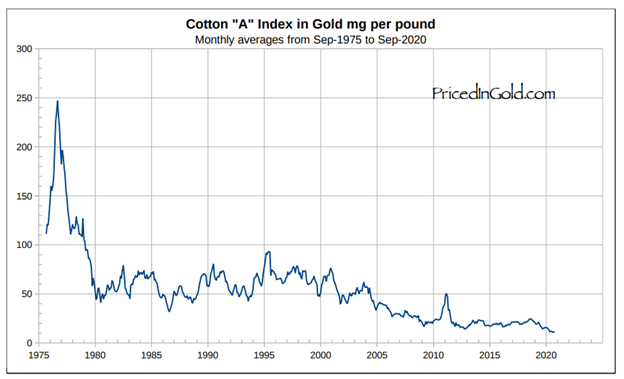

Clothes are really cheap right now, as retailers dump tons of unsold stock from the 2020 fashion ranges onto the market at bargain prices. If you already have enough clothes, fine, but if not, it might be a good time to ensure you do, especially clothes to see you through cold winters. With this glut, it’s hard to know what will happen to all elements of the clothing supply chain in the future: Cotton farmers, Garment manufacturers, and clothing retailers.

The low price of cotton has already made it hard for growers in countries like India to turn a profit and it’s hard to know how they are coping with this huge change in market conditions. There’s been talk of suicides in the media. With cotton at an all-time low, we can assume that prospects are not great for some cotton farmers.

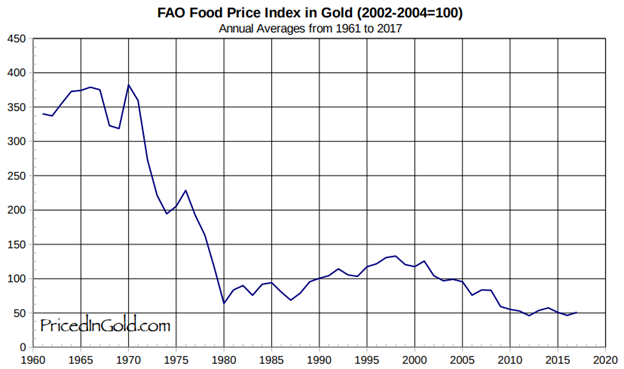

100 years ago, the average household spent up to 50% of its income on food. Today, that figure is nearer 10%, giving us all more disposable income for consumer goods, bigger mortgage repayments, and exotic holidays. Food is cheap, almost too cheap, in fact. As some farmers struggle to turn a profit and big supermarkets control the supply chain.

(Chart showing food prices as a proportion of income)

Of course, some of this is due to technological improvements in farming and manufacturing, but much of it is due to fiat currency inflation versus gold. Perhaps it can’t last forever – we may well already be being prepared for future food shortages and increases in food prices. You may have already noticed shortages during the crisis or increases. On a personal level, visiting the supermarket regularly, a 20-25% increase in fruit, vegetables, and dairy products has occurred since March 2020, when Corona began. That’s interesting, as these products are all the ones with the shortest shelf life, that are most immediately impacted by price rises. Others, like dried, tinned and frozen goods, may be in huge stock at warehouses down the supply chain behind the supermarket facade, and price rises may take longer to feed through. Observe these headlines from recent times, as to what they may be planting the seed in your head to germinate for:-

“UK potato farmers fear another washout for this year’s crop. “

The Guardian, August 2020

“Bread price may rise after dire UK wheat Harvest.”

BBC News, August 2020

“Coronavirus: Meat shortage leaves US farmers with ‘mind-blowing’ choice.”

BBC News, May 2020

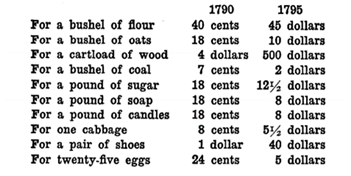

If you wonder how far food prices can rise during a monetary crisis, then here is an example of prices from “Fiat Money Inflation in France,” an excellent study of the hyperinflation that occurred there during the French revolutionary times, which coincide with the decline of the French empire before the handover to Great Britain.

Now, how well covered are you for those kinds of price rises in basic commodities, the essentials of life?

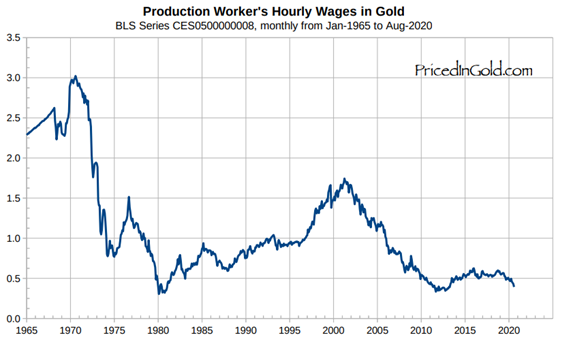

First, let’s get the really bad news out of the way. You’re probably extremely underpaid for what you do. In fact, you probably get paid around one-sixth of the salary that a worker got in 1970 for the same job. There has been a huge real decline in income, masked by fiat currency inflation, meaning many of us are worse off than ever.

This goes a long way to explaining why life has got harder and most households now require both parents to go out to work to keep the family going. A less common occurrence back in 1970.

To look at this another way, to return to 1970, our salaries need to increase by six times. Yes, six times. Imagine that, a world that rewards work and self-sufficiency over clever monetary tricks. Sadly, such a world is not here yet.

“We Should Be Happier To Have A Job Than To Have Savings”

– Christine Lagarde, 2019.

Thank you, Christine. Your quote is the main reason why “How to Invest in Gold and Silver” got revisited 13 years after the original publication. Gold had underperformed for many years after attaining an all-time high in 2012, and gold mining companies had declined massively. Meanwhile, stock markets were apparently flying along and hitting new highs daily. Commodity prices were now lower than ever, in many cases and there was doubt in the premise of that book still being valid. Perhaps the 2008-09 crisis and fallout really was over?

When Christine said that, though, it was time to wonder. For those who don’t know Christine Lagarde, she makes big decisions on finance at the ECB (European Central Bank). The ECB is the banking facet of the European Union, and she was appointed to lead it in 2019. It doesn’t seem to matter that she was convicted of a financial crime 4 years earlier, nor did she seem to suffer any penalty for the conviction. Christine attends many events where big-ticket items are discussed, but no agenda or minutes of meetings are made public – think Bilderbergs and the World Economic Forum, for example. Christine even has Hollywood links – she was interviewed in 2010 as part of the documentary “Inside Job,” helping explain how those awful banks played roulette with our mortgages, savings, and investments, and it was all their fault. Lone financial gunmen, acting alone.

In summary, Ms Lagarde is a big cheese – or fromage grande to use her own language. When she says something, you can believe it may not just be her own words and possibly comes from somewhere deeper.

So ask yourself now, what does this quote mean to you? Images of savings being destroyed and life being a treadmill of working to earn enough to survive? Working on this premise, but not knowing what was coming or how that would be achieved, it was hard to know what to do except ensuring you have some diversification, then watch and wait.

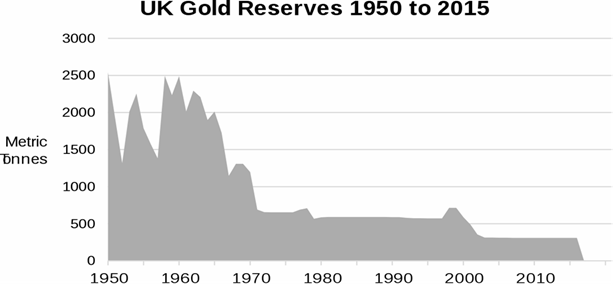

Once governments got you used to the concept of using just one currency in your everyday transactions and got you used to the trust that they were looking after your gold – they began loaning it out and selling it off, often without your knowledge or consent.

(Chart: source: Wikipedia By Tsange – CC BY-SA 4.0)

Looking at the chart, it’s easy to see the UK gold reserves have declined massively, especially in the 1960s – leading to the famous ‘Pound in your Pocket’ speech by Prime Minister Harold Wilson in 1967, trying to assuage voters that their pound was still worth a pound, as the value plunged against other currencies. A pound of what, Harold? In 1999, the UK decided to sell off over half the nations’ remaining gold reserves, some 400 tonnes. At the time, gold was at the end of a major 20-year bear market, and the price was at an all-time low, a price last seen in the 1970s. The Bank of England, the custodian of the countries’ gold reserves, insists that it was never consulted in the decision, and some leaks, in fact, suggest that many of their staff vigorously opposed the move. They claim that Her Majesty’s Treasury and them alone made the decision. At the time, the Chancellor of the Exchequer was a Mr. Gordon “Golden” Brown, who subsequently became Prime Minister.

Even worse, the huge gold sales and auctions were publicly announced well in advance, thus giving gold dealers the chance to prepare for the glut of gold that was about to be released onto the market, and force the price down still further as a result. The normal strategy is to keep intended government gold sales quiet, then simply conduct the sales on the open market, obtaining the best prices possible, then announce the results afterward.

Why might a government decide to sell off one of the main assets of its people at the lowest price possible? There were rumours and accusations that the gold was sold to prevent top Hedge Funds who had got it wrong gambling on the price of gold from going bust and destroying the worldwide economy, among others.

Regardless of the truth of the rumours, 1999-2002 has subsequently been proved to have been exactly the right time to start buying gold, not selling it; in fact, the value of the gold sold by the UK has risen by over ten billion dollars since that time. This period in gold price history is now referred to as ‘The Brown Bottom.’

While the owning of gold was illegal for US citizens from 1933, the USA sat atop international trade after World War 2, allowing gold convertibility at the same price of 35 dollars an ounce for other nations. This was called the ‘Bretton Woods’ agreement, referring to the location where it was signed. However, partly due to the cost of paying for the Vietnam War, the number of dollars in circulation began rising in the 1950s and 1960s. Nations like France and West Germany seized their chance to exchange their devaluing dollars for the real thing, gold at $35 an ounce. In 1971, the window for exchanging gold was officially closed.

Founded by Paul Tustain, BullionVault sits somewhere between Goldmoney, for safety and Gold storage, and more traditional trading services. Bullionvault is UK-based, although an additionally interesting feature is the ability to store your gold in their New York, London or Zurich gold vaults. Dependent on which country you are a citizen of, you will probably feel most comfortable placing your gold outside of that country so that is not subject to your local government jurisdiction, so top marks for considering that feature.

An interesting aspect of the three separate vaults is that these could be considered as separate currencies in their own right. For example, if at some point in the future there was a repeat of the 1930s US Gold confiscation, gold stored in a New York Vault might become priced significantly lower than gold stored in a Zurich vault, as US holders try to sell and place their gold outside their own jurisdiction.

BullionVault allows you to buy and sell Gold on their impressive looking trading platform, where buyers and sellers of gold from each vault can meet and state their required selling/buying prices, so if you are more inclined to hold gold, occasionally sell on a dip, then buy in again later, then this could well be the best service for you.

Their fees for transactions and monthly storage are really low too, so they are very worthy of investigation. The storage fee is currently $4 per month fixed, regardless of holding size, and only payable for the months in which you held Gold.

Again, Bullionvault has proved popular with Gold Bugs accumulating gold for the future financial crisis they believe is in the offing.

Payment into BullionVault is by bank transfer. Payment out is by bank wire transfer to your chosen bank account.

In recent years, they introduced a silver option. That they took so long may have been something to do with BullionVault being UK-based and the UK charging VAT on silver sales, which could, to many observers, seem to be another example of government getting in the way of free trade.