The natural consequences of this? Inflation, even if it takes a few years for the currency to begin circulating, or the death of the pound? Take your choice.

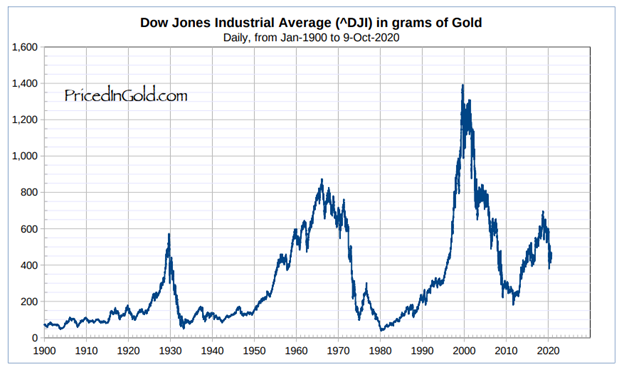

Now for more news, your stock market investments may be worth under one-third of their value in 2000. Gasp. Yes, the gain of the last 20 years has been illusory. For sure, some countries and some market sectors have done better than others, but for the USA main index, this is exactly what has happened.

(Chart: DJIA priced in ounces of gold)

Even if large corporations prosper, the US DJIA stock index and gold have a history of a near meeting when a financial crisis bottoms out. Currently, the DJIA is worth around 14 times the price of an ounce of gold. In 1932 and 1980, just over one ounce of gold bought the DJIA. Whether a large stock market crash achieves that, as was the case in 1932, or inflation pushing up the gold price, as was the case in 1980, it may be destined to happen again.

Oil is still one of the biggest building blocks of life. Regardless of whether you now work from home instead of driving to work every day in the gas-guzzler or not. It’s used in everything – fuels, plastics and pharmaceuticals, to name a few. In fact, if you now work from home, chances are you’re turning up the winter thermostats a bit more often than you would at work. You’re probably also buying a lot more food from the supermarket, most of it encased in plastic packaging. Even if your heating system is not oil-based, oil remains one of the main fuels available for generation of electricity, and could well do so for many, many years, regardless of how many windmills they build.

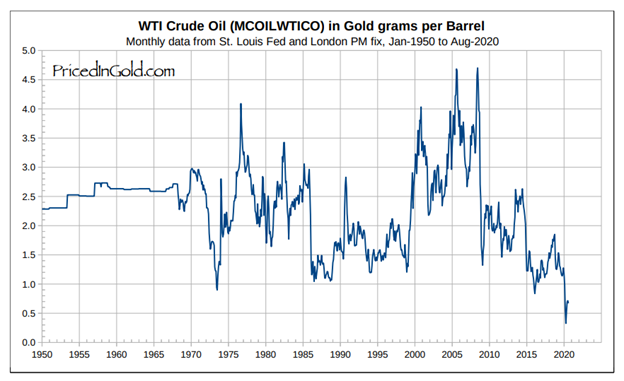

So, the good news. You’ll be pleased to hear is that oil is at an all-time low, when measured against gold. Luckily enough, since with your earnings being one-sixth of the 1970 value, you may not be able to afford to keep the house warm or drive a car otherwise. Any apparent price rises you see at the pumps are merely an inflation of your fiat currency.

Now for the bad news, can it continue?

Maybe not. For many years, gold and Oil actually maintained a near 10:1 ratio relationship.

(Chart: Gold/Oil ratio 2010 to 2020)

As the chart shows, this relationship has become distended as a result of the Corona crisis. There’s now a near 50:1 relationship as of August 2020. This may imply oil is actually quite cheap, gold is expensive, or that the ratio no longer holds. There has been a multitude of media articles heralding the death of oil. However, it seems to have missed the attention of many that all of this data – everyone’s Facebook posts, Instagram images, or cloud software solution is stored on a server somewhere that requires electrical power to run. For sure, in the case of one Instagram post, that electrical consumption is miniscule, but multiply it across a world of 7 billion people, and you get an idea now of the immense electrical power required. Oil, natural gas, and coal are still heavily used in electrical power generation across the globe.

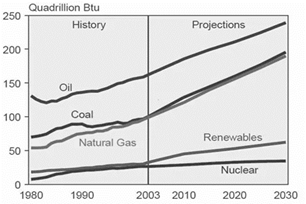

(Chart: Actual and predicted power sources to 2030)

The eagle-eyed among you may have spotted the chart dates from 2003. This was deliberate since more recent data shows it to be correct. If so, the future trend for oil consumption is still upward.

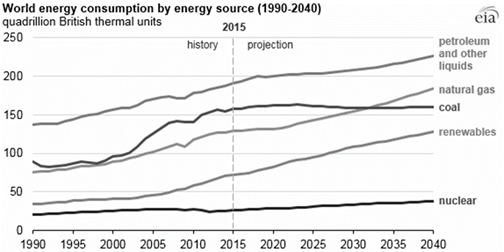

(Chart: Energy consumption to 2040)

So, and this is only a question, not investment advice, maybe oil itself is not finished yet as an investment. If not, could it revert back to the 10:1 ratio with gold and if so, at what price for both?

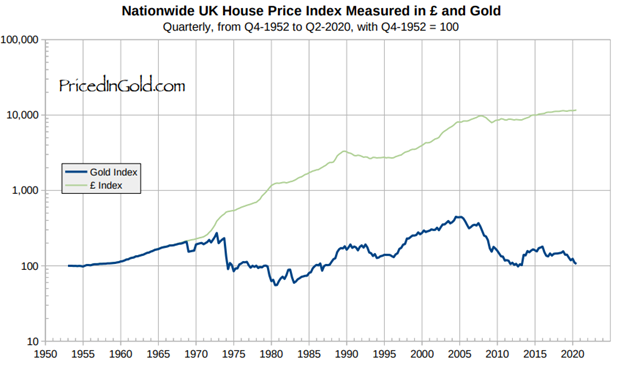

Now for some big news. If you live in the UK, your house topped in value in 2005 and has been falling ever since. In fact, it’s now about one-quarter of what it was worth then. What? I hear you say. Okay, yes, in fiat currency units it has gone up, but measured in gold, it has fallen dramatically.

Measured this way, house prices are very close to the 1950 mean. However, with the Corona crisis still in full swing, employment uncertainty for many and wages still at one-sixth of their 1970 value, it’s entirely possible the market could still have a lot further to fall. Conversely, if something happens to get wages closer to the mean or inflation rises, well, they could easily move upwards in fiat currency terms especially.

In this case, the housing market is hard to exit, unless you prefer the uncertainty of renting. Everyone needs to live somewhere.

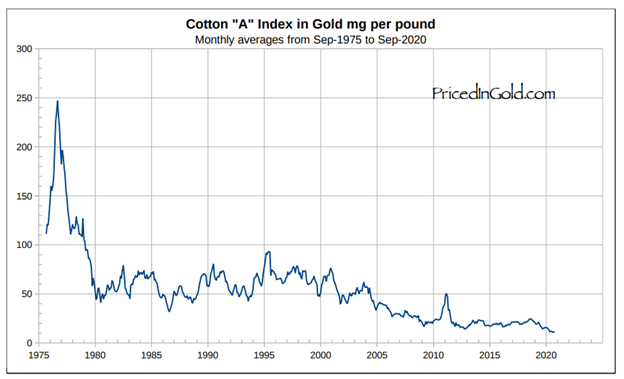

Clothes are really cheap right now, as retailers dump tons of unsold stock from the 2020 fashion ranges onto the market at bargain prices. If you already have enough clothes, fine, but if not, it might be a good time to ensure you do, especially clothes to see you through cold winters. With this glut, it’s hard to know what will happen to all elements of the clothing supply chain in the future: Cotton farmers, Garment manufacturers, and clothing retailers.

The low price of cotton has already made it hard for growers in countries like India to turn a profit and it’s hard to know how they are coping with this huge change in market conditions. There’s been talk of suicides in the media. With cotton at an all-time low, we can assume that prospects are not great for some cotton farmers.

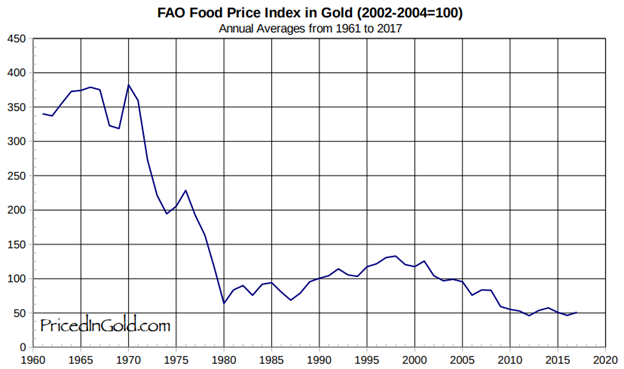

100 years ago, the average household spent up to 50% of its income on food. Today, that figure is nearer 10%, giving us all more disposable income for consumer goods, bigger mortgage repayments, and exotic holidays. Food is cheap, almost too cheap, in fact. As some farmers struggle to turn a profit and big supermarkets control the supply chain.

(Chart showing food prices as a proportion of income)

Of course, some of this is due to technological improvements in farming and manufacturing, but much of it is due to fiat currency inflation versus gold. Perhaps it can’t last forever – we may well already be being prepared for future food shortages and increases in food prices. You may have already noticed shortages during the crisis or increases. On a personal level, visiting the supermarket regularly, a 20-25% increase in fruit, vegetables, and dairy products has occurred since March 2020, when Corona began. That’s interesting, as these products are all the ones with the shortest shelf life, that are most immediately impacted by price rises. Others, like dried, tinned and frozen goods, may be in huge stock at warehouses down the supply chain behind the supermarket facade, and price rises may take longer to feed through. Observe these headlines from recent times, as to what they may be planting the seed in your head to germinate for:-

“UK potato farmers fear another washout for this year’s crop. “

The Guardian, August 2020

“Bread price may rise after dire UK wheat Harvest.”

BBC News, August 2020

“Coronavirus: Meat shortage leaves US farmers with ‘mind-blowing’ choice.”

BBC News, May 2020

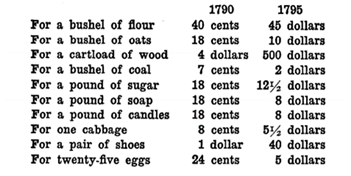

If you wonder how far food prices can rise during a monetary crisis, then here is an example of prices from “Fiat Money Inflation in France,” an excellent study of the hyperinflation that occurred there during the French revolutionary times, which coincide with the decline of the French empire before the handover to Great Britain.

Now, how well covered are you for those kinds of price rises in basic commodities, the essentials of life?

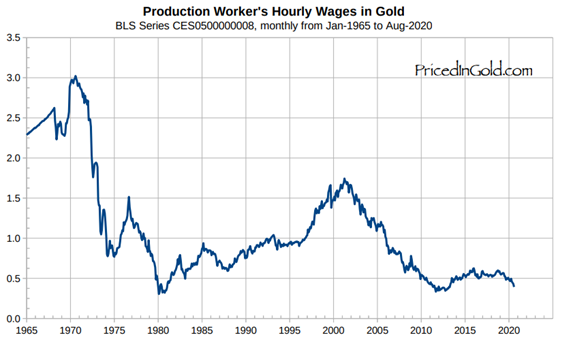

First, let’s get the really bad news out of the way. You’re probably extremely underpaid for what you do. In fact, you probably get paid around one-sixth of the salary that a worker got in 1970 for the same job. There has been a huge real decline in income, masked by fiat currency inflation, meaning many of us are worse off than ever.

This goes a long way to explaining why life has got harder and most households now require both parents to go out to work to keep the family going. A less common occurrence back in 1970.

To look at this another way, to return to 1970, our salaries need to increase by six times. Yes, six times. Imagine that, a world that rewards work and self-sufficiency over clever monetary tricks. Sadly, such a world is not here yet.

The whole Corona crisis has also shown how digital the world has become concerning money. The furlough scheme is a major example in itself. UK Businesses were expected to log their furlough claims using the internet. The IT infrastructure and software to support this was in place in record time – major IT projects can often take months or years to design, develop, thoroughly test, and release. It’s then an example of how the currency can now be distributed quickly to millions, through the central government, to businesses, then distributed electronically to customer accounts in banking computers. Not a single physical coin or note ever having existed.

Many other nations introduced a furlough scheme, but the USA did not. In this case, they mailed out Corona stimulus cheques of $1,200 to everyone. Lamenting, while doing so, that it was a shame that it was taking longer because they needed to get signatures on every cheque. Then, that it would have been so much easier had they had more direct banking details, such as a nominated bank account, to send the money out to the recipients electronically.

As to spending, well, more and more of it became electronic as internet shopping took off even further. Still, some preferred physical currency to a certain extent. However, one of the early casualties of Corona has been cash – the number of shops now insisting on electronic payments only and media stories saying that cash can help spread the disease is a clear signal that the system no longer wants people using old-fashioned coins and notes. Also, remember Gresham’s law about bad money forcing out good? There is probably a case that people are genuinely retaining more banknotes and coins at home, just if they are needed for some kind of emergency. However the Corona crisis goes, it doesn’t seem like good news for savers or freedom.

The Corona / COVID-19 crisis has invented a whole new multitude of ways to distribute money to favoured interests and individuals. In addition to being unemployed, you can now get your full salary for doing nothing, while someone else you worked with has to continue to do their job, on the same salary, with all of the commitments their job requires. In the UK that has become known as ‘furlough’. In many cases, it goes way beyond those in employment – the self-employed can also make claims to get their earnings covered. Staying at home, being paid full salary, having all the time in the world to do the house up, improve the garden, or even find another job to boost your earnings even more – a concept in the UK that has become affectionately known as “double-dipping.” It all sounds idyllic, doesn’t it, but there must be a catch, and, of course, there is.

If the various schemes introduced to pay employed people to do nothing sound like a major extension to the welfare system, then that’s probably because they are. Some people were bound to question the point in being productive, when for the same amount of money you could do nothing. Not everyone will feel that way, and some will be upset and stressed about the loss of work, but in terms of bending minds, taking power from people, and getting them used to rules, it is very reminiscent of the 1980s deindustrialisation of Northern England. A period when hopelessness and despair took over from community, self-sufficiency, and a strong work ethic. The schemes may also be the start of something that has been thrown around for several years now and never gained traction – Universal Basic Income. The concept of Universal Basic Income (UBI) is quite simple – every citizen is issued with a basic amount of government fiat currency per year, enough to live on. It never caught on because too many people could see through it – whatever the UBI level is, it would become the new zero, and self-sufficiency and freedom would surely be eroded. To say nothing of the existing gold base supporting more and more newly issued currency units every year.

Where the extra fiat currency has come from to fund all this, it is hard to see any real statistics on. We know that at some point, public borrowing must rise, and indeed, that is being presented through the news to make it palatable to the public, but increasing borrowing takes time. Wherever it came from, the consequence of these policies must be Inflation. Quite simply put, there must be a lot more currency units in circulation than there were a year ago, and even if the majority of those units are in bank accounts right now, doing nothing, at some point, they will begin to enter the market and circulate. At that point, prices must begin to rise. Whether this happens tomorrow or in a few years seems to be the only question.

The Medical Care 2020 app is growing so big; it’s taking up all the resources on your smartphone. In the future, it may even store your COVID-19 test pass certificate, too, along with Microsoft’s proposed ID 2020 inoculation history – if there’s space. You may have to show them to be able to even travel, attend a football match or concert, should those things ever open up again.