On the 3/3 a woman called Sarah, aged 33, was murdered by a man in London. A policeman, as it happens. I don’t claim the credit for spotting that one, but it does lead into some interesting coincidences, especially considering how the story has been used way beyond being a murder case that should be investigated with respect for everyone until…no, innocent until proven guilty and policing with logic instead of emotion seems to have gone by the wayside.

Amongst the media circus for everyone to invest their emotion in, there were even calls from some for a curfew for all men to be home by 18:00. That supposed believers in a free society think it’s okay that one incident like this should ride on the rights and livelihoods of 60 million-plus people is bizarre. However, it fits with the whole Corona regime that we are entering a Minority Report-style world where everyone is believed to be infected unless proven otherwise and now, everyone is believed to be guilty unless proven otherwise. Anyway, didn’t they miss the other big question it raises – who’s going to enforce this curfew if something so extreme was ever allowed to happen? The Police?

If there is anything to really be gained from this story, it’s surely that the police themselves cannot be trusted. I fear however, that even this will be used against humanity. All it needs is someone to say humans can’t be trusted to police each other…if only there was some way a computer, with it’s impeccable logic and lack of prejudice could do the job. Maybe a robocop or robodog? Let’s just forget for a moment that computer software is always programmed by humans, with huge margin for error. Robocop from the 1980s was rather prescient in seeing how it could go.

Meanwhile, journalism seems keen to focus on the alleged perpetrator still receiving his salary while suspended from his job. Even helpfully repeating across the globe how he will still receive his at least £33,000 salary. Here, here and here. What a bizarre figure to concentrate on. Unless…..dipping into the world of freemasonry, Google tells me there are 33,000 lodges worldwide, with 33,000 members in many lodges. Continuing the search theme, other newsworthy stories further feed the conspiratorial fires. It’s amazing how many COVID-19 injections seem to be delivered in batches of 33,000. Utah, for example, a home of alternative religion and mystic rites certainly seems keen on the magic number. Gibraltar just completed it’s injection programme too, although this media source doesn’t seem to be in on the numerical importance. Then we have the shooting in Georgia, also successfully being used to whip up racial and gender division where there previously was none, with this story helpfully telling us that the alleged perpetrator came from Woodstock, Cherokee county with a population of…33,000.

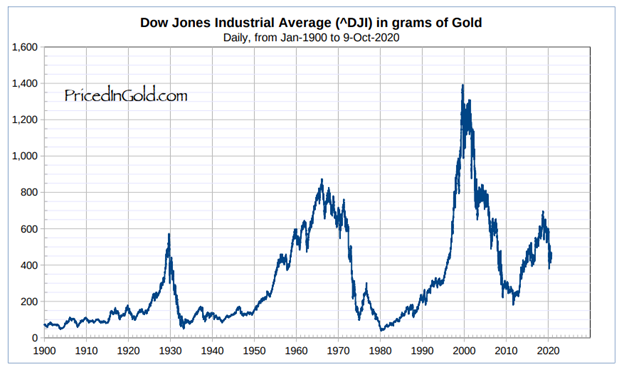

Why am I bringing all of this up, do you ask? Returning to the world of finance, let’s finish with the biggest 33,000 financial sign going. Amongst all these 3’s the world’s biggest stock market, the DOW Jones Industrial Average hit an all-time high last week. I don’t need to tell you what it was before you visit the link, do I? The Federal Reserve even helped out, the story tells us, with soothing words and promises of further stimuli to keep the party going, despite the reality of every economic indicator. I find myself wondering if words and actions may diverge soon. At least for a little while until other parts of the agenda are enacted.

I shall leave the final words to De La Soul, with their 90’s hit, although apparently that was a cover of Schoolhouse Rock / Bob Durrough in 1973. Meanwhile, we can all ponder what the 33,000 signifies to those in the know, along with asking the how and why of Wayne Couzens’ black left eye.